Of the many ills of the Buhari administration, Nigeria’s rising debt profile boggles the mind. Debt is important for a cramped mono-economy like Nigeria. It helps the country metaphorically dump its scooter and buy a tricycle, dispose of the tricycle, and buy a car. However, when debt is misused, it could lead to palpitations.

A sizeable chunk of Nigeria’s debt portfolio comprises multilateral credits from the World Bank and the International Monetary Fund. The overall trend history of multilateral debt repayments suggests that satisfaction is far from a foregone conclusion. They are serviced over a long period of time, say 35 to 40 years and are often cancelled or, to use the technical term, forgiven. According to one analysis, Nigeria has only paid 21.66% of the value of loans it has collected from the World Bank since the first borrowing in 1947.

For economies at the top of the power pyramid, the cost of borrowing money from lenders is very cheap. They could pay the principal of that loan annually, along with maybe a 1% interest rate – before 2022, at least, when interest rates were hiked in reaction to the war in Ukraine. The United Kingdom had a 101% debt-to-GDP ratio as of the last quarter of 2022, compared to Nigeria’s 23.20%. It is not prohibitively expensive for the UK to borrow beyond its GDP because it is cost-effective for the government, and the productivity of the world’s sixth-largest economy supports consistent debt service. But for the Russia/Ukraine War, it is not commonplace for these big boys to pay so much in debt servicing. While the UK’s debt service to revenue for 2022/2023 was 13.55%, that of its wealthier younger sibling, the USA, stood at 9.713%.

When the cost of servicing debt becomes consistently higher than revenue, the default alarms start sounding. Two African countries, Ghana and Zambia, have already defaulted – failed to meet their debt service obligations as and when due. This was the charge given to Nigeria’s Debt Management Office when it was established in 2000 – to stop the Nigerian economy from reaching a state of debt overhang. Debt overhang describes a situation where a country’s future earnings cannot service its debts. However, the Buhari-led administration plunged Nigeria into a precarious debt position, one that markets and many political watchers consider being one of the biggest challenges for the new Bola Tinubu government.

Let’s take a look at the debt situation.

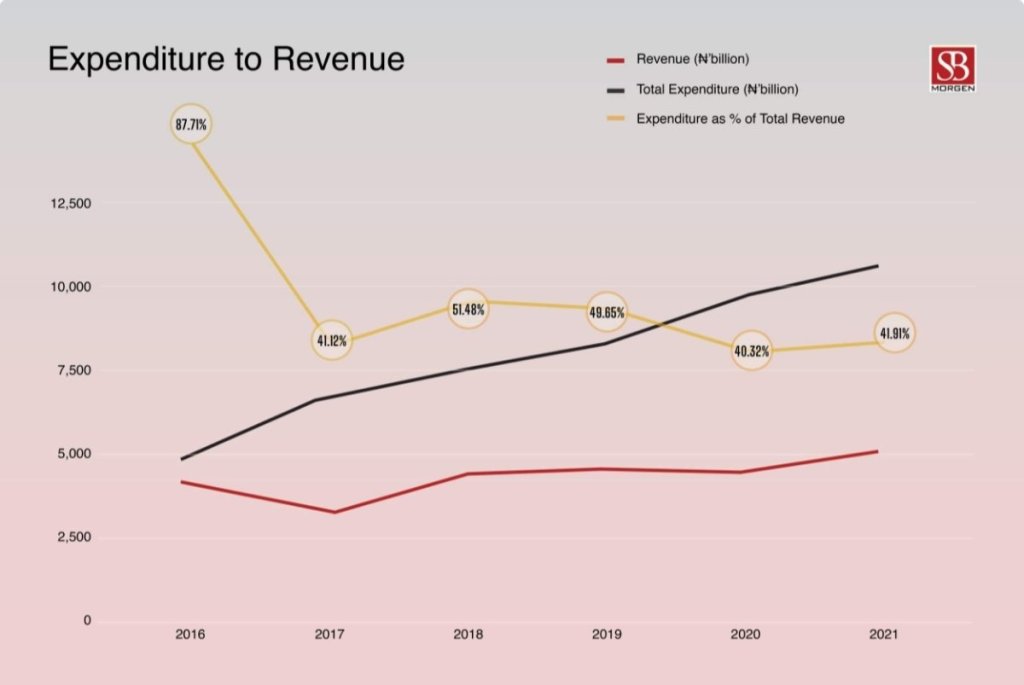

From July 2015 to December 2022, the federal government and its counterparts at the state level, who have struggled to pay salaries, borrowed ₦34.13 trillion. That excludes the ₦23 trillion in Ways and Means spending authorised by the Central Bank of Nigeria for the federal executive. From 2016 to 2021 (the years in which the budget office has published comprehensive data) the federal government earned revenue totalling ₦23.18 trillion. Contrastingly, the federal executive spent ₦47.77 trillion as reported by the budget office in December of the reference years. 2016 was an outlier. The budget office reported ₦5.36 trillion in expenditure as of December of that year. In its 2017 fourth-quarter report, it alluded to a much lower estimate of ₦4.4 trillion. When 2016—where the government raised 87.71% of what it spent is taken out—the federal government only pulled in up to 50% of its budget estimate once – in 2018.Chart: Revenue as a percentage of total expenditure. Data source: Budget Office of the Federation.

The new government realises it is in a bind. Speaking to the new members of Nigeria’s 10th Assembly, budget office head Ben Akabueze insisted that the country now has “minimal borrowing space, not because our debt to GDP is high, but because our revenue needs to be more significant to sustain the size of our debt.” He insisted that “once a country’s debt service ratio exceeds 30 percent, that country is in trouble, and we are pushing towards 100 percent, and that tells you how much trouble we are in.”

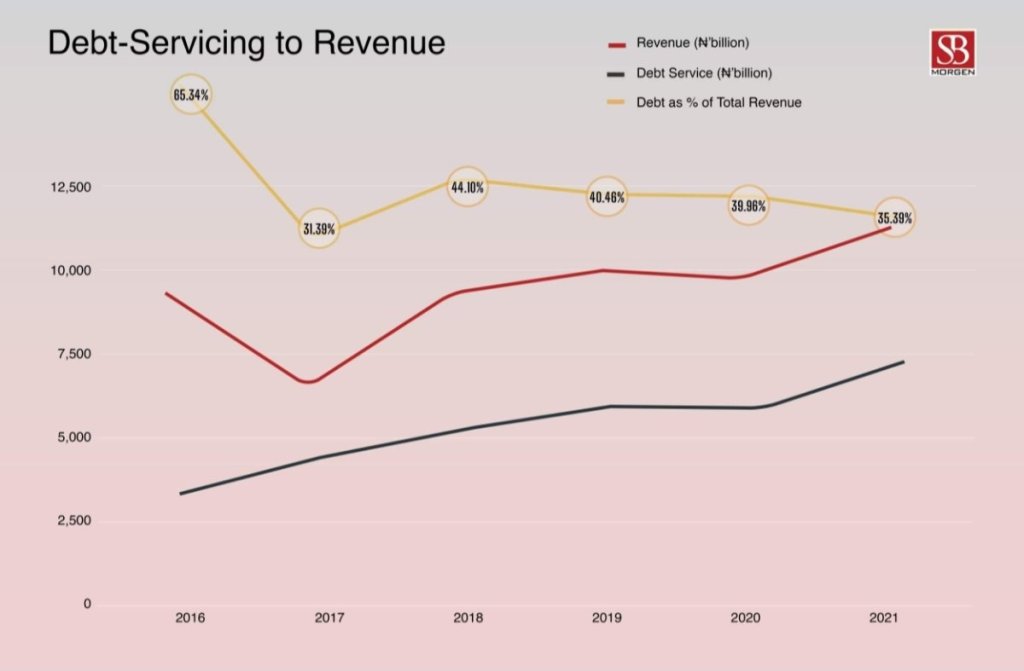

Mr Akabueze’s office shows that apart from 2016, when the debt service to revenue was, on average, ₦34.66 of every ₦100 the government earned, the Buhari administration in a typical year spent over ₦50 of its revenue servicing loans. Other independent sources think this ratio is much higher.Chart: Debt-servicing to revenue. Data source: Budget Office of the Federation.

President Buhari pulled every lever, including dispensing with aspects of the rule of law to fund his governing priorities. In the process, he handed President Tinubu a cramped economy with almost no wiggle room for debt-funded expansion on such priorities as infrastructure. In 2017, Nigeria’s self-imposed debt-to-GDP ratio was 19%. It was extended to 25% by the end of that year. In 2021, the ceiling was raised to 40% to accommodate the flush of Ways and Means spending. Bloomberg now estimates that Nigeria’s debt will reach ₦80 trillion by the end of this year, meaning we may be reaching the helm of the ceiling.

The initial moves of the new administration have put investors and market watchers in a positive mood on the expectation that a more business-friendly Aso Rock is in the offing and much-needed reform, or at least steps in the right direction, is on the horizon. With the tough hand handed to the present crop of policymakers by the previous administration and the significant political and economic goodwill required to push through the required reform, these stakeholders might be best advised to lower the bar of expectation a few notches.

Culled from SBM Intelligence

Leave a comment